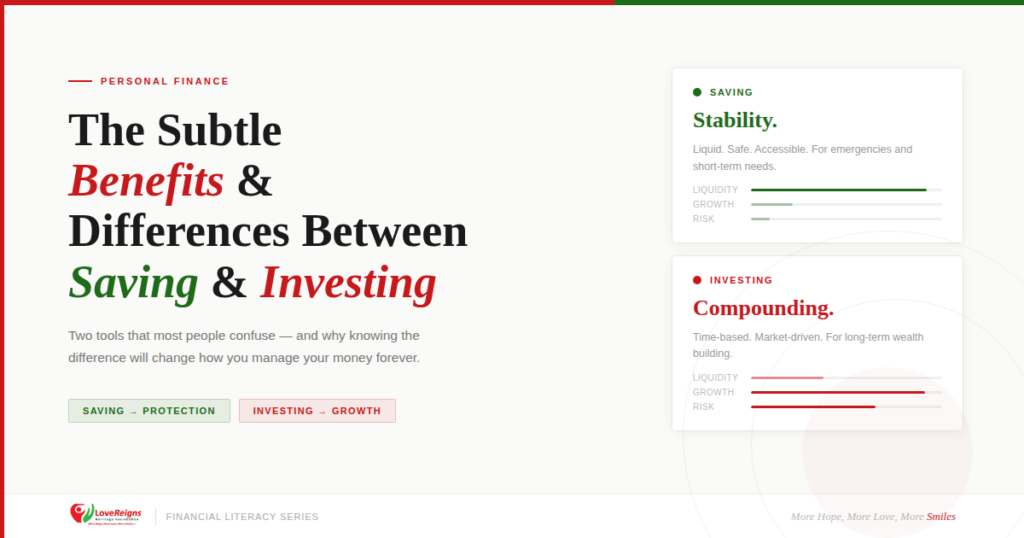

The Subtle Benefits and Differences Between Saving and Investing

Most people treat “saving” and “investing” as synonyms for the same habit. They’re not. Each has its own place, and they both should be done. For example, you can save a portion of your income and feel safe, but it doesn’t grow. Or you invest money you might need next month, and end up frustrated when life throws an emergency bill at you. One keeps you safe while the other builds wealth. Using them interchangeably or skipping one entirely are among the financial mistakes people make. Here’s how to think about both clearly. Saving Is for Stability, Not Growth When you save money, you’re essentially setting cash aside in a place you can reach quickly, such as a bank account, a fixed deposit with short tenure, or somewhere low-risk and liquid. The purpose is stability. You save so that when your car breaks down, or a family member needs help, or you lose a client for two months, you don’t have to borrow or sell something you didn’t plan to sell. Saving is your financial buffer against life’s unpredictability, which it always is. The trouble is that many people treat savings like an investment. They pile money into a savings account, watch it earn 3-4% interest annually, and feel like they’re building something. They’re not in the long run. Inflation chips away at that balance. If prices are rising at 15% a year and your savings account pays 4%, your money loses purchasing power every month it sits there. Saving keeps you protected. It does not make you richer. Investing is where growth happens. When you invest in stocks, mutual funds, real estate, index funds, or a business, you’re putting money to work in a way that’s meant to outpace inflation over time. The mechanism behind this is compounding: your returns generate their own returns, and given enough years, the numbers stop being linear and start looking geometric. Someone who puts ₦50,000 into a diversified mutual fund at 25 and leaves it alone will almost certainly have more at 45 than someone who starts at 35 with twice the amount. Time is the difference. The money had more years to compound. This is why people who invest earlier tend to end up further ahead, even when they earn less than their peers who delayed. Investing only makes sense with money you won’t need anytime soon. If you invest your emergency fund and the market dips 20% the same month your landlord raises rent, you either sell at a loss or scramble to cover the rent. That’s the trap of mixing the two up. What this looks like in practice Let’s say you earn ₦350,000 a month from salary, freelance, small business, whatever the source. A reasonable split might look something like this: After covering your necessary expenses (rent, food, transport, obligations), you have about ₦100,000 left to work with. Of that, you could direct ₦40,000 into savings, building toward three to six months of expenses in a stable, accessible account, and ₦60,000 into an investment vehicle, such as a mutual fund or a dollar-denominated asset, if you want some currency protection. The savings portion just sits there. But it’s doing a job: making sure you never have to liquidate your investments at the wrong time because an emergency shows up. In a nutshell, the investment portion is the part that, five or ten years from now, will look meaningfully different from what you put in, assuming the market does what markets have historically done over long periods: grow. Why do people delay, and why does that delay compound too There’s always a reason to wait. The month isn’t good. There’s a wedding to fund, school fees, and a business expense that came up. These are real pressures, not excuses, and anyone who dismisses them hasn’t met a real budget. But the delay has a cost that’s easy to underestimate because it’s invisible, it’s the growth that didn’t happen, the years of compounding that didn’t start. What tends to work is automating both. When money moves into a savings account or investment fund before you see it in your main balance, you stop seeing it as available. People who automate these transfers consistently end up with more saved and more invested than those who plan to do it manually at the end of the month, because the end of the month has a way of arriving with nothing left. eMBED code for mailer: Newsletter Signup for news and special offers! Subscribe Loading… Thank you! You have successfully joined our subscriber list.